Investment Returns

Apply discount rates to compare opportunities

The final step of building a financial model is choosing a discount rate. Discount rates are the Cost of Capital or Hurdle Rate that an investor requires to earn on similar types of investments when factoring in all the forms of risk.

Discount rates are applied to the entire set of cash flows over the life of the investment and are not only applied to the reversionary value.

Before choosing a discount rate, it is important to keep in mind the purpose of the financial model. Is the model an investment valuation for a specific investor, or is it a market valuation for the general market? The answer to this question will determine which party's discount rate your analysis will be using.

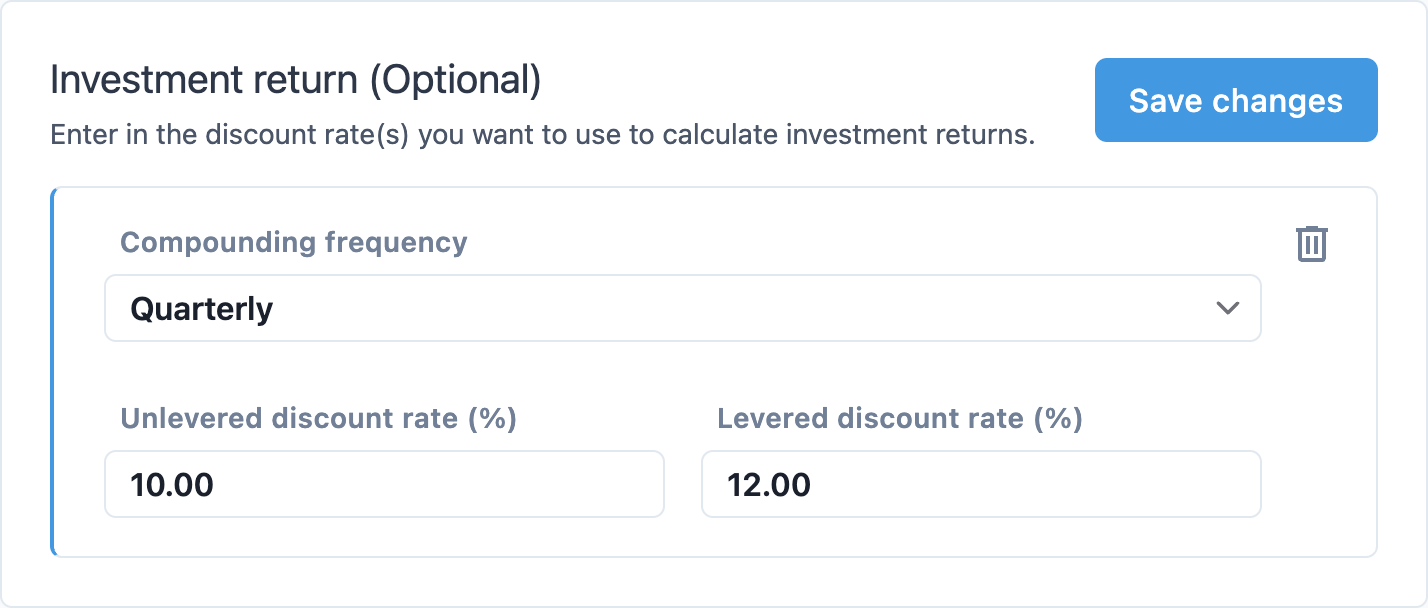

A discount rate requires two pieces of information: the nominal annual discount rates and the shared compounding frequency.

Adding return information

Compounding frequency

The compounding frequency converting the nominal discount rates to real rates, factoring in the effect of compounding.

Compounding options:

- Annual

- The discount rates compound once per year on the analysis start anniversary.

- Semiannual

- The discount rates compound twice per year, every six months after the start of analysis.

- Quarterly

- The discount rates compound four times per year, every three months after the start of analysis.

- Monthly

- The discount rates compound twelve times per year, every month after the start of analysis.

Unlevered discount rate

Input as a percentage, the nominal discount rate the investors would expect without the use of debt financing.

Levered discount rate

Input as a percentage, the nominal discount rate the investors would expect when factoring in the additional risk from the use of debt financing.

The levered discount rate should always be equal of higher than the unlevered discount rate since adding leverage to an investment can add a meaningful amount of risk.