If you're an office owner running a stabilized flex space–whether you've branded it yourself or partnered with an operator–you've likely faced the same frustrating disconnect: You've filled your space. You're earning more money than if you filled your space with a conventional lease. But when it comes to valuation and borrowing–you're still treated like a traditional office owner.

More than one valuation method

When it comes to valuations, it's important to remember that there isn't a single valuation method–it's more of a toolbox. Yet because of the long-term nature of the traditional office lease, we fell into the habit of reaching for the same old tool every time. For decades, every problem was a nail, so we reflexively reach for the direct capitalization hammer. But of course, not every situation is a nail.

Here's a pattern we've been seeing more and more: An office owner adapts to weaker demand for traditional long-term leases by some combination of reducing unit sizes, shortening commitment terms, delivering CAT A+ fit-outs, and layering on services like IT, cleaning or even beer taps.

Whether it's called serviced office, managed office, plug-and-play, or coworking, it's all variations on the same themes: the tenants get higher flexibility, invest less upfront CapEx and receive more services–and in return, the building owners earn higher revenue per square foot.

Win-win ... but there's a catch: The extra income—the premium above what the space could earn through conventional leases—is often excluded from the property's value.

In general, there is some recognition that the premium income is worth something–but now the debate is about how much value to apply to the new income.

Enter the Top Slice method

The Top Slice method is a simple, defensible approach that lets you reflect the full performance of a stabilized flex property without overstating value or stepping outside accepted valuation practices.

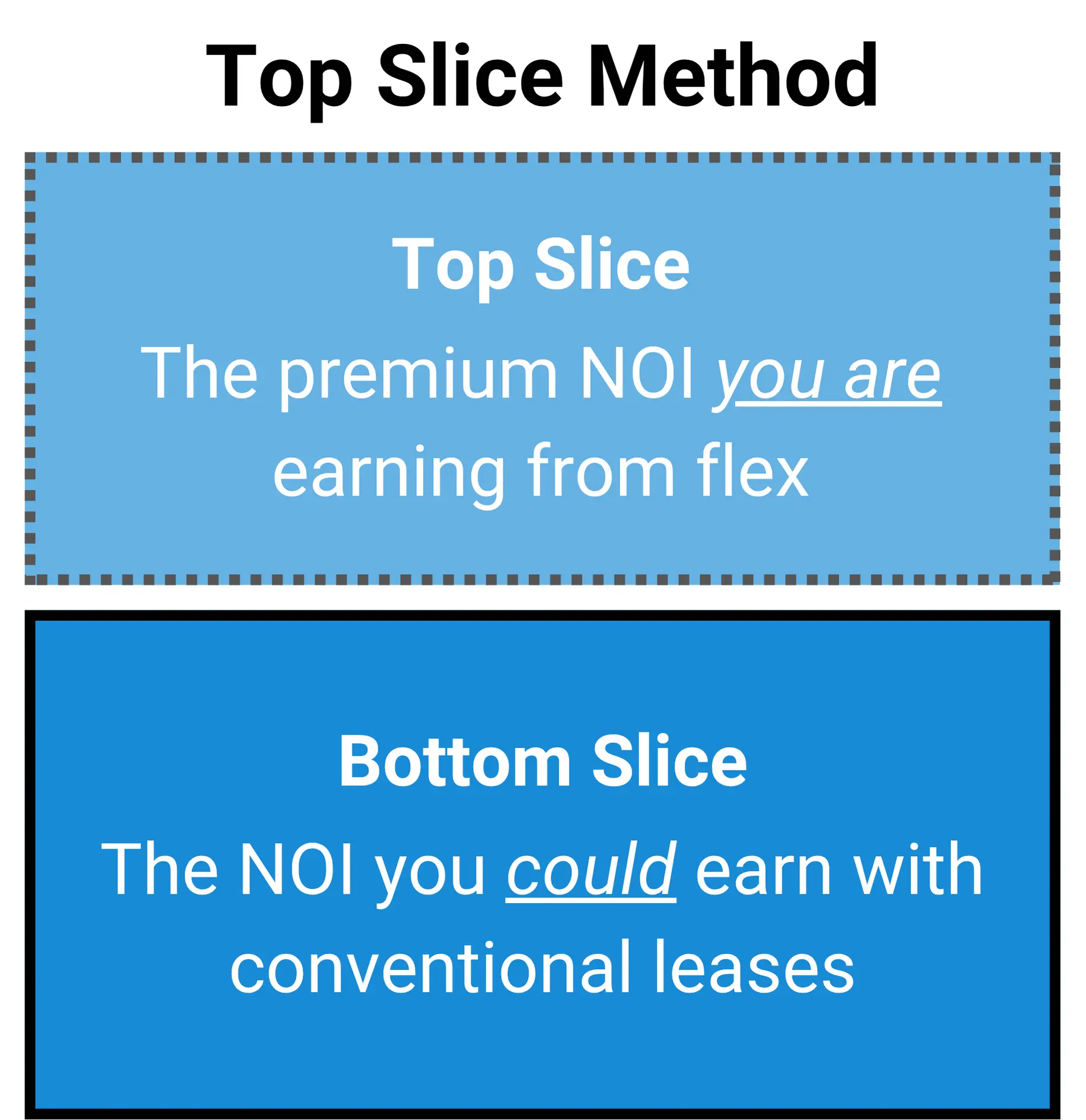

I was first introduced to the Top Slice method through the work of Andrew Skinner at Savills. One of the best things about the Top Slice method is how simple it is: subdivide the income stream based on its risk and value each part, then add them together.

For a stabilized flex property, the Net Operating Income (NOI) could be split into two slices:

- The bottom slice is the NOI the property would theoretically earn with conventional leases

- The top slice is the premium NOI you are earning from flex.

Each slice is then capitalized separately using a different rate that reflects its risk:

- The bottom slice gets a lower cap rate (stable, long-term)

- The top slice gets a higher cap rate (riskier, performance-based)

The final step is to add the two values together. The result is a valuation that is based on real estate valuation fundamentals, captures the operator's contribution and stands up to investor, lender, and auditor scrutiny.

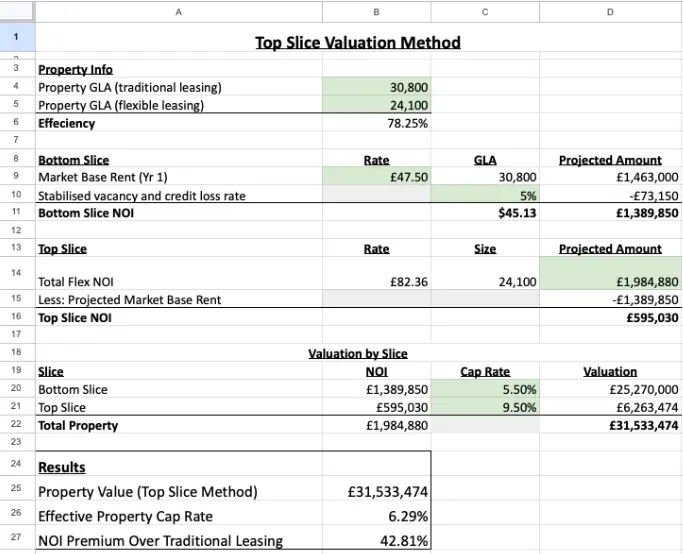

Example: Tanner's House

Let's say we have a property in the Bermondsey area of Southwark that theoretically could earn £1,390,000 in NOI if leased traditionally. However, a few years ago we decided to convert it to a fully flexible leased property which is now earning a stabilised NOI of £1,985,000 per year.

To value the property using the Top Slice method, its NOI would be split into two distinct slices:

- A bottom slice of £1,390,000 (the theoretical NOI if leased conventionally)

- A top slice of £595,000 (the total NOI £1,985,000 minus the bottom slice of £1,390,000)

To determine the value of the property, each of the NOI slices would be capitalized at different rates. In our example, let's assume that similar properties with traditional long-term office leases have traded at a 5.5% capitalization rate while flexibly leased properties have traded at a 9.5% capitalization rate.

- Bottom slice value of £25,273,000 (£1,390,000 divided by 5.5%)

- Top slice value of £6,263,000 (£595,000 divided by 9.5%)

Using the Top Slice method, the value of the property would be £31,536,000 calculated by adding the value of the two slices together.

Explore the Top Slice Method with ReturnSuite

To see the full Tanner's House model in ReturnSuite (free), log into ReturnSuite and open the Tanner's House sample property. From there you can inspect the rent roll, leasing assumptions, NOI and cash flows. Adjust the inputs and watch how your cash-flow predictions change.

Then download our free template spreadsheet and combine it with your custom ReturnSuite results to run your own Top Slice valuation.

When the Top Slice method works best

The Top Slice method isn't just a way to value flex internally–it's a way to make the value defensible. But like any tool in the valuation toolbox, it works best in certain situations.

1. The property is stabilized

The Top Slice method assumes the property is performing, not an untested model. Your property needs to be earning a predictable income–month after month–and you can point to consistent occupancy and operating results. If you're still in startup mode or relying on aggressive projections, you're better off with a discounted cash flow (DCF) or expected value model.

2. There's a realistic bottom slice

To make the method work, you need a credible estimate of what the building could earn under traditional leasing–the base case NOI. This doesn't require current leases in place–just a defensible market rent and occupancy level that reflects what the space could achieve if you walked away from flex tomorrow.

If that fallback scenario isn't realistic–say the layout is too specialized or demand for traditional leases is gone–you're going to need to make adjustments. Potentially, you could factor in the costs to revert to traditional leasing, including void periods and leasing expenses.

3. You can cleanly separate income streams

The method works best when you can clearly distinguish the slices of NOI. If your income is blended beyond recognition–or relies too heavily on a unique system–it may be too hard to apply this approach and have all the value be attributed to the property alone.

Ideal use cases

Owner-Operators

The building owner also runs their own flex operation under a proprietary or in-house brand. This is the cleanest use case for the Top Slice method, as the owner has full visibility into both sides of the income.

The bottom slice is based on fallback traditional leasing income that the building would earn if leased conventionally. The top slice is the incremental NOI from the flex model: higher occupancy, higher rates, and any margin from services.

Lease Arbitrage Operators

The operator signs a long-term lease with the building owner, then runs a flex operation, subleasing space short-term and earning a spread. Since the two entities are at complete arms-length and don't share revenues, the slices aren't added together. However, the Top Slice methodology can still be applied.

The bottom slice becomes the lease-backed income stream valued with a traditional capitalization rate. The top slice captures the flex income uplift. If the lease is long enough and the location has proven performance, the operator may be able to build a defensible valuation around that spread, especially when raising capital, refinancing, or preparing for exit.

Management Agreements

In this model, the building owner partners with a third-party flex operator and earns a combination of a base return (often a fixed or minimum payment) and a share of upside, typically structured as a revenue or profit share. This structure often resembles retail leasing with turnover rent—where the base rent might be below market, and the variable portion can be meaningful but volatile.

The bottom slice can be made up of either the contractual minimum or what the property could earn if leased conventionally. It is likely more defensible to use the conventional leased values to reflect the asset's fallback value that aligns with standard valuation practice.

The top slice would be any property owner share of income above that of the fallback market rent and capitalized at a higher rate to reflect its variability and reliance on operator performance. This creates a valuation greater than simply capitalizing the minimum guarantee and ignoring the upside.

Key Consideration: If the market rent fallback is unrealistic (e.g. the building's layout only works with flex), then the fallback assumption needs to be adjusted–or the valuation may need to be adjusted downwards to reflect the capital needed to achieve the fallback rent.

A more accurate way to value stabilized real estate

With flex leasing becoming more wide-spread, including flex income in property valuations is becoming more important.

The Top Slice method helps you do just that–by separating what the property could earn through traditional leases from what it's actually earning today. The method is transparent, risk-adjusted and grounded in accepted real estate valuation practices.

And most importantly, it gives investors, lenders, and stakeholders a clear view of both the stability and upside of your property–the ultimate role of a valuation.