Your CFO knows you’re cherry-picking. End the financial debate and focus on the strategic decision.

You've done the hard work. You've toured the buildings, evaluated the layouts, consulted with your team, and narrowed it down to two viable options that could each work for your business.

Then your CFO asks: "Which one is cheapest?"

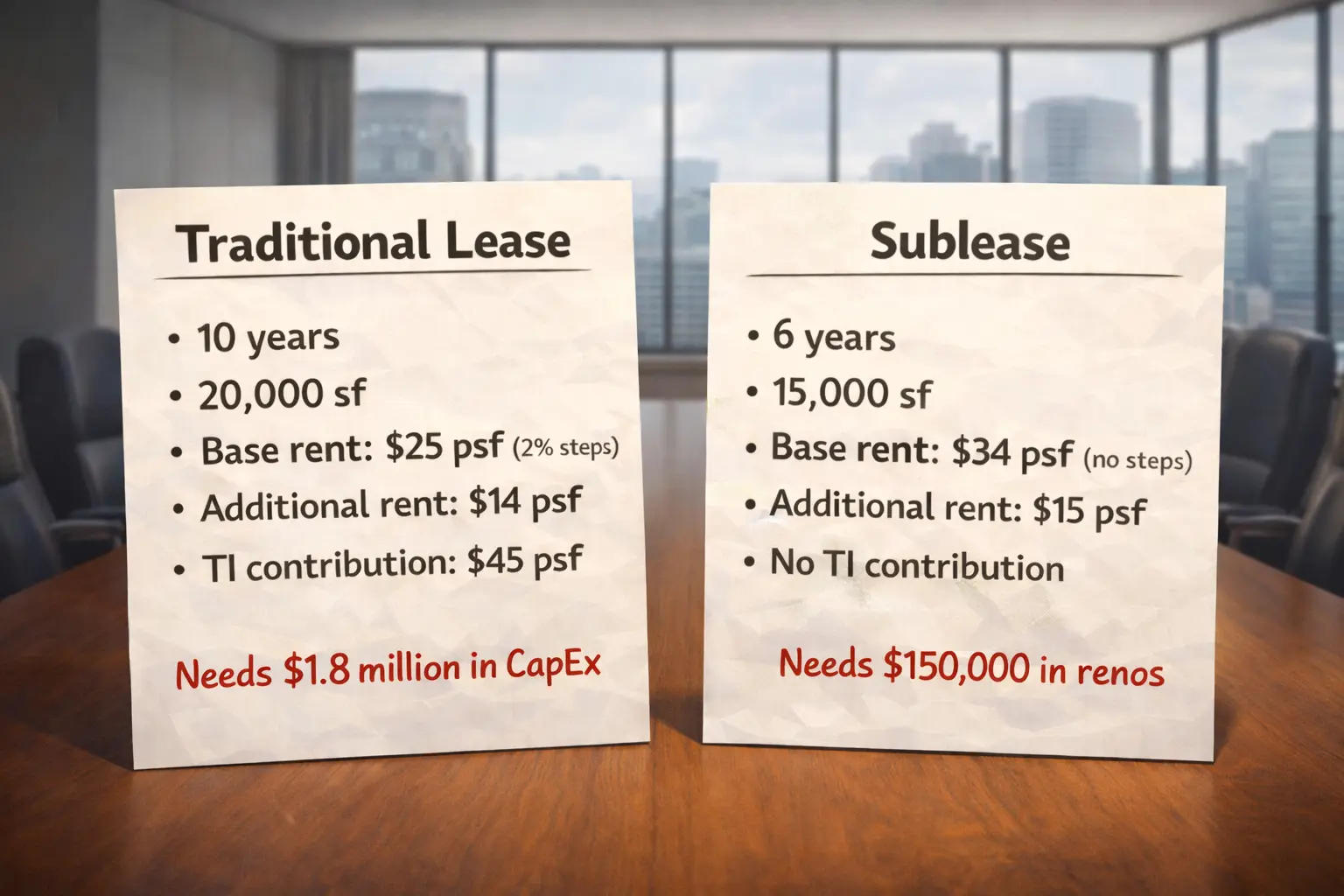

The traditional lease is cheaper per square foot...but the sublease has a lower first year cost since very few tenant improvements are needed. The total annual costs of the sublease are less...but the traditional lease is cheaper in the later years.

You could make either of them look cheapest and your CFO knows this. They've seen the game before. So whatever number you lead with, they're going to question your methodology, challenge your assumptions, and ask why you didn't use a different metric.

The financial debate takes over and the strategic conversation never happens.

But that's not the conversation you want to have.

Why these conversations are so hard

Here's why these conversations are so hard: you're trying to evaluate strategic features while simultaneously arguing about financial comparison.

"The sublease puts us in the same building as our largest client" gets mixed with "but the cost per square foot is higher" and "the commitment is shorter" and "we'd avoid having to invest in tenant improvements."

You're comparing bundles without knowing what each actually costs—like choosing a phone plan without seeing the monthly bill.

What you actually need is a way to answer two separate questions:

Question 1 (Financial): Which option costs less when you account for everything—all cash flows, timing, the cost of capital and commitment length?

Question 2 (Strategic): What do the other options offer that might justify paying more?

Right now, you're trying to answer both simultaneously. That's why the conversation gets stuck.

What you want is to walk in and say: "This option is objectively the cheapest—and for only $X more per month, we get these specific benefits. Is that premium worth it?"

The first step is to separate the financial from the strategic. But to do that, you need one thing: a single financial number that accounts for everything—one that's comparable across different term lengths, incentive structures, and upfront costs. A number your CFO can agree with, so you can spend your time on the question that actually matters.

The single financial metric

There are plenty of ways to put a financial number on a lease, but they all ignore something important.

- Rental rate per square foot is the most common—but it ignores commitment length and the capital required to make the space usable.

- Total lease value captures the full financial commitment—but longer leases will almost always look more expensive, making short-term options appear deceptively cheap.

- Net Present Value factors in your cost of capital—but like total lease value, it unfairly penalizes longer commitments, making direct comparison across different term lengths unreliable.

The problem isn't the math—it's that none of these metrics account for everything simultaneously.

Ultimately, a lease is a financial obligation in exchange for the use of an asset—no different from any other capital investment decision. It generates a lumpy, irregular stream of cash flows: rent payments, operating costs, tenant improvement spending, free rent periods, each landing at different points in time across commitments of different lengths.

The solution is to treat it like one.

Take every cash flow, account for its timing, adjust for your cost of capital, and convert the whole thing into a single comparable number: the Equivalent Monthly Debt Service (EMDS)—what each option actually costs you per month when everything is accounted for.

The same way your carrier converts a confusing bundle of data, calls, hardware financing, and contract length into a single monthly bill—then asks: for an extra $15 per month, would you like international calls included?

One number per option. Directly comparable regardless of term length, incentive structure, or upfront capital requirements.

What EMDS reveals

Here's what both options actually cost when you account for everything:

- The traditional lease option has an EMDS of $53,686 per month

- The sublease option has an EMDS of $59,189 per month—a $5,503 per month premium over the traditional lease.

Now you can focus on strategy

Once you have EMDS, you've answered the financial question. The traditional lease costs $53,686/month. The sublease costs $59,189/month.

The traditional lease is financially optimal.

Now you can focus on the strategic question: what does the sublease offer that might justify paying $5,503/month more?

What you get for that premium:

- Immediate occupancy (no construction delay, no lease overlap)

- Same building as your largest client

- Right-sized for your team without excess space

Is being in the same building as your key client worth $5,503/month? That's $66K/year.

If it helps you close one additional deal, shortens your sales cycle, or strengthens the relationship, the ROI is obvious. If proximity doesn't materially impact the client relationship, save the money and take the traditional lease.

This is strategic decision-making: clear baseline cost, explicit pricing of strategic features, rational evaluation of whether the premium delivers value.

Not defending your discount rate assumptions—but deciding whether client proximity is worth $66K/year to your business.

ReturnSuite calculates EMDS for lease decisions—so you can separate financial comparison from strategic evaluation.